DAO Strategy and Legal Wrappers

Jun 08, 2022 | chrisbrummer, rodrigoseira

Contents

One of the important features of Web3 is the way in which blockchain-based technology enables individuals to organize themselves in novel arrangements to make problem solving potentially more creative, efficient and communitarian.

DAOs are a case in point. In contrast to the 20th century industrial corporation reliant on the separation of ownership by stockholders, and centralized control by managers and directors, DAOs offer a radically different template for organizational participation: one where ownership and control can merge–driven by smart contracts, fluid memberships, and transparent transactional channels1.

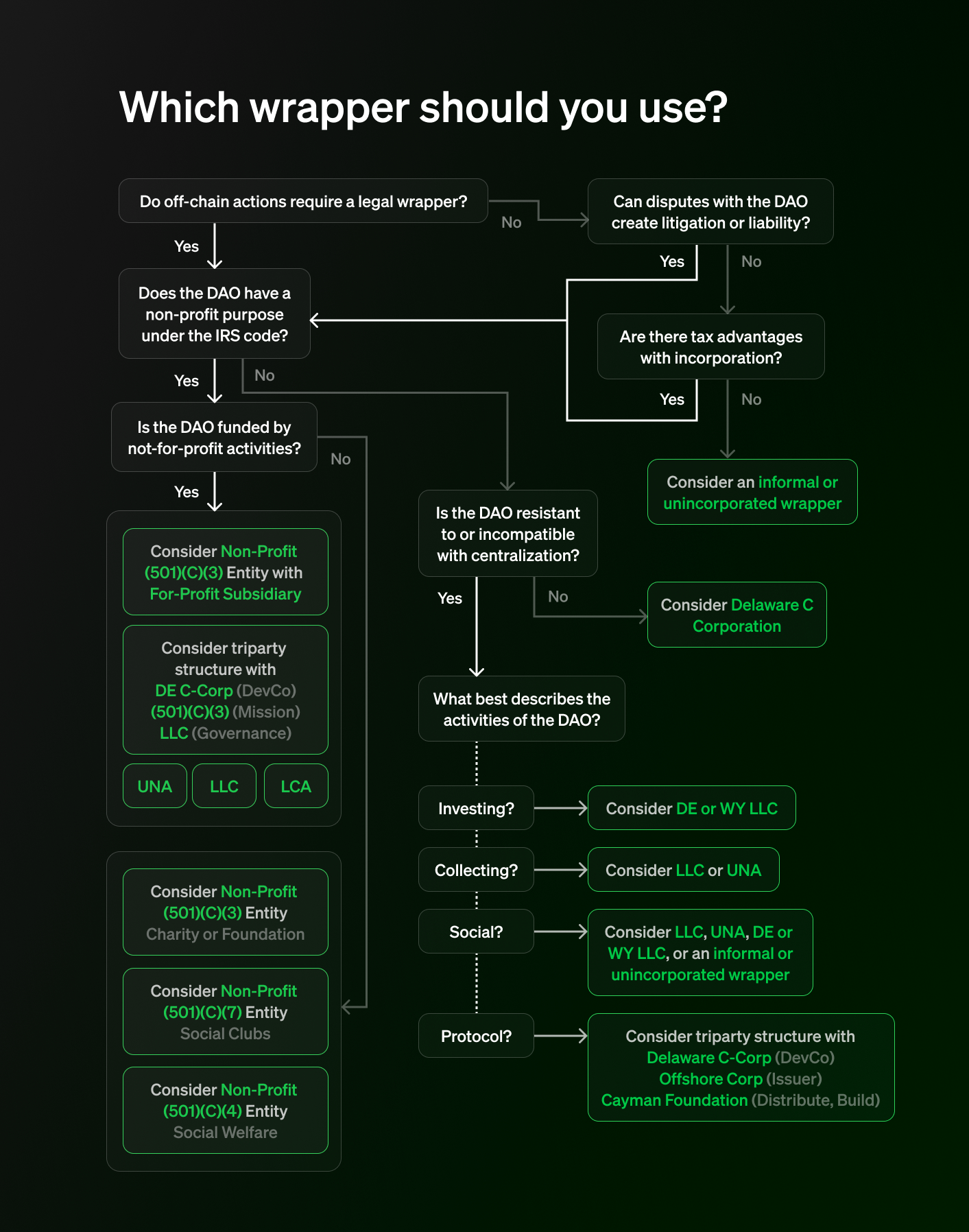

But building a DAO involves more than just code; it also requires skillful legal engineering to enable the DAO to operate in the real world and protect builders and contributors. Yet the range and complexity of DAO legal structures can leave the best engineers (and their lawyers) dumbfounded. So in this post, we summarize our new white paper Legal Wrappers and DAOs, which offers founders (and policymakers) the first comprehensive overview of legal wrappers–and pairs it with a framework for understanding how these legal elements interact with the purpose and operations of popular DAO applications.

Strategic Considerations

The spectrum of potential DAO wrappers is broader than many founders likely assume. It spans legal entities and forms commonly associated with business associations to both incorporated and unincorporated nonprofits. Yet even in this variety, we anticipate that most founders will have to engage a similar process of reasoning when it comes to choosing legal wrappers.

Key considerations will include the following factors:

- The scope and purpose of a DAO’s operations;

- The legal risk and tax liability associated with the DAO’s operations;

- The size and permanence of the DAO’s membership;

- The degree of decentralized governance employed; and

- The resources of the DAO.

Scope of DAO’s operations

The need for a legal wrapper will largely hinge on whether the DAO’s sponsors intend for the DAO to interact with the real world, and whether the DAO’s activities create potential legal and tax liabilities for its members.\n\nAlthough informality carries enormous benefits for DAOs in terms of speed and cost, commercial transactions off chain frequently run on legal rails. From opening a bank account and hiring lawyers and accountants to hosting IRL events, a formal legal identity is often necessary. Sponsors and founders of DAOs will have to think concretely about the scope of the DAOs operations, not only on-chain, but also off, and make an assessment as to whether out of pure practicality a legal wrapper will be necessary.

Legal wrappers are also, at their core, risk reduction tools. Informality leaves members with few legal protections should the DAO or DAO members become subject to lawsuits for negligence or other failures. Founders will have to evaluate these risks–and consider whether or not the activities of their DAO, or proposed DAO, create potential scenarios for liability, and by extension exposure to DAO members and participants. While no one can predict the future, the potential liabilities of a DAO that is limited to a token-gated discord channel vary fundamentally from those of a DAO that controls a protocol with billions of dollars TVL.

Sponsors of larger, more ambitious projects will have to give additional consideration to whether the DAO’s activities create any tax liabilities that if left unprepared could undermine or even threaten the financial health of the project. If a DAO is generating revenue that could be deemed taxable income – including for example from token sales, treasury diversification, or staking – founders should analyze who may be liable for tax on that income and whether forming a legal entity could result in a clearer understanding of who bears that liability and may allow for better tax treatment.

Degree of decentralized governance employed

Every type of legal wrapper involves some points of centralization and dependence on outside actors. DAOs should consider the extent to which their operations can, and are willing to, accommodate centralization, and in what ways. Notably, legal wrappers offer a broad spectrum of choices as to the degree to which governance is evenly distributed among owners, members and investors. DAOs and their advisors will have to undertake a careful internal assessment of their purpose and objectives, and carefully analyze the extent to which legal wrappers can accommodate DAO token holders directing or influencing the actions of any persons operating the legal wrappers without raising the risk that the legal entity is disregarded by a court or that control results in tax or other liability.

Membership

A DAO’s membership, both in terms of its size and its fluidity, will determine the available and adequate legal wrappers.

Early on, DAOs will have to assess the long term arc of their operations. Many legal wrappers are limited in the number of members they can accommodate due to federal laws and regulations, often to numbers far smaller than the number of members of some of the most prominent DAOs2. However, DAOs with large numbers of members can still leverage other types of legal wrappers, and even use traditional structure as “siloed” entities meant to isolate specific liabilities or for other purposes.

The fluidity with which members will join and exit the DAO is also a consideration that will affect which legal wrappers will be most advantageous. Many legal entities require their shareholders or members to execute contracts and reveal their identities in order to legally join the entity and may not be available to DAOs that seek to have a large, decentralized and pseudonymous membership base that is determined on the basis of ownership of a freely tradable token. However, there are some legal wrappers that may accommodate more fluid memberships and other “ownerless” entities such as foundations or special purpose trusts that can serve specific purposes, such as serving as a vehicle for future grantmaking. Such wrappers, however, may be novel and carry more legal ambiguity as to how they operate in practice.

US-related activities

The extent to which a DAO’s members and activities are in the US will also affect the range of legal wrappers that are available. Some offshore legal wrappers, such as an ownerless foundation or special purpose trust, may not be available or tax efficient for projects with significant US-connections. Conversely, projects that don’t have a significant US nexus may want to avoid relying on US-based legal wrappers in order to lower tax and liability exposure in the US. DAOs should therefore design the governance mechanisms controlling their legal wrappers to ensure that they don’t inadvertently hamper the effectiveness of their legal structure.

Resources of the DAO

From a practical perspective, DAOs should consider how much of their resources they want to devote to their legal structure. As noted above, there are no perfect solutions and in order to be effective, complex DAOs will likely need a bespoke structure – and this can quickly get expensive. A potential option is to start with a simple structure which is further developed over time, as the scope of the DAO’s activities grows, and so do the resources at its disposal.

Legal Wrappers (A Quick Overview)

Once founders understand the strategic considerations applicable to their DAO, the next step is to analyze which legal wrappers might be most adequate. We provide an in depth analysis of these wrappers in our white paper, but here’s a quick, and very broad, overview:

Unincorporated General Partnership

One of the risks of operating a DAO without a legal entity is the DAO being deemed an unincorporated general partnership. While this theory has yet to be proven in a court and it has faced some criticism, it could potentially result in DAO members being liable for other members' liabilities or those of the DAO.

Corporations

The most common type of traditional legal entity can be helpful to isolate tax and legal liability for DAO projects, but has some limits in terms of its structure (e.g., it requires centralized governance in the form of a board of directors, etc.), membership and also subjects DAOs to US tax. They have been leveraged as DevCos, or as siloed entities which are affiliated to the DAO and intended to block a specific liability or other special purpose (such as a subDAO).

LLC

LLCs are also widely used in the traditional context, but offer more structural flexibility than corporations in terms of their governance. LLCs can be member-managed and allow members to waive their fiduciary duties to each other, making them more adept to decentralized governance. Some states have even passed specific DAO LLC laws that are intended to facilitate a DAO’s operations. However, DAOs with very large or fluid memberships will be limited in their ability to use LLCs and even a member-managed LLC will have certain points of centralization (e.g., a tax representative).

Nonprofit Options

DAOs with charitable missions could also look to form a nonprofit entity and have it designated as tax exempt in the US. This route provides the DAO with legal personhood and important tax benefits, but limits a DAOs range of activity and ability to distribute profits to its members. Some projects have used multi-entity structures that incorporate for-profit and nonprofit entities.

UNA

Unincorporated non-profit associations are the non-profit equivalent of an unincorporated general partnership, but in certain states can provide its members with limited liability and can also file with the IRS to be taxed as a corporation. UNAs also potentially offer a more flexible framework to facilitate a fluid membership. While UNAs are limited in distributing profits back to their members, they can engage in some for profit activities (this may, however, disqualify them from tax-exempt status). One downside to UNAs is that their implementing statutes can vary widely from state to state and there is little case law, making potential outcomes hard to determine.

Co-Ops

Co-ops are a form of legal wrapper that has a long history in the US and provides an alternative to the traditional corporate model that separates ownership and control by typically requiring all members to be both owners and direct contributors to the co-op. Certain states have passed more modern Co-op frameworks that allow for investor members and variations from the one-member one-vote standard which have led to some DAOs experimenting with this entity type.

Ownerless Foundations

Ownerless foundations are a form of legal wrapper available in certain offshore jurisdictions that acts like a trust that is controlled by a board or council which can in turn be directed by the vote of the DAO. The foundation can be used to make grants to further the development of a protocol. However, the DAO members will not be owners of the foundation or “wrapped” by that entity. There are some limits on the control that US-based projects can exercise on offshore foundations in order to maintain their tax advantages and other liability protections.

Special Purpose Trusts

This legal wrapper is a type of trust available in certain offshore jurisdictions which can be created by transferring assets to a set of Trustees which can in turn act as instructed by the vote of the DAOs token holders. The Trustees are supervised by an Enforcer who can bring suit if they act improperly. It is similar to the ownersless foundation in that it can be used as a vehicle to custody and distribute assets as well as enter into legal agreements. One perceived advantage of this structure is that it does not require any governmental filing to be formed, as it is purely a creature of contract between the person contributing the assets and those that will act as their stewards.

1 Adolf A. Berle and Gardiner C. Means, The Modern Corporation and Private Property (New York: Harcourt, Brace & World, [1932] 1968).

2 For example, to qualify as an investment club, which is how several venture DAOs have avoided the need to register as an investment company (a virtually impossible task with most DAO structures), there must be no more than 100 members. (see reference). If a DAO is leveraging a private company in the US (such as a Delaware C-corporation) as part of its structure, it should be mindful that membership thresholds can also require it to register as a reporting company (requiring costly disclosure and potentially more liability). (see reference)

Disclaimer: This post is for general information purposes only. It does not constitute investment advice or a recommendation or solicitation to buy or sell any investment and should not be used in the evaluation of the merits of making any investment decision. It should not be relied upon for accounting, legal or tax advice or investment recommendations. This post reflects the current opinions of the authors and is not made on behalf of Paradigm or its affiliates and does not necessarily reflect the opinions of Paradigm, its affiliates or individuals associated with Paradigm. The opinions reflected herein are subject to change without being updated.